Use Case Summary

| Industry | Life insurance, accelerated underwriting, digital distribution |

| Problem | Self-reported body data can be inconsistent or misrepresented; in-person measurement steps slow down accelerated underwriting |

| Solution | Guided mobile body scan from two smartphone images |

| Outputs | Structured body-related measurements and verification signals |

| Role | Supporting evidence for underwriting review — not standalone decisioning |

| Business value | Faster evidence collection, better triage, stronger fraud-prevention support |

Introduction

Accelerated underwriting has helped life insurers reduce friction, shorten application timelines, and move more applicants through digital journeys. But faster underwriting also creates a practical evidentiary challenge: insurers still need reliable ways to evaluate body-related risk signals when applicants no longer complete every step in person.

Self-reported height, weight, BMI, and build data can be incomplete, inconsistent, or intentionally misrepresented. For life insurers, this directly affects risk classification, pricing accuracy, fraud exposure, and case routing — and the gap widens as digital distribution scales.

The market signal is clear. In 2025, 92% of consumers researched life insurance online, and 52% said they were inclined to buy a policy issued through accelerated underwriting. Swiss Re reports that some markets now process up to 90% of applications through automated underwriting engines, with the global average around 75%. The National Association of Insurance Commissioners (NAIC) has also highlighted the continued expansion of accelerated underwriting since 2020–2022 and ongoing oversight of insurers’ use of external data, predictive models, and artificial intelligence.

Mobile 3D body scanning provides a practical support for addressing this evidence gap. Using a guided smartphone scan, insurers can collect structured body-related data remotely and use it as supporting evidence within accelerated underwriting, applicant verification, and underwriter review workflows.

Disclaimer. Mobile 3D body scanning can support underwriting workflows and evidence collection, but it does not provide diagnoses, replace required medical evaluations, or make clinical judgments.

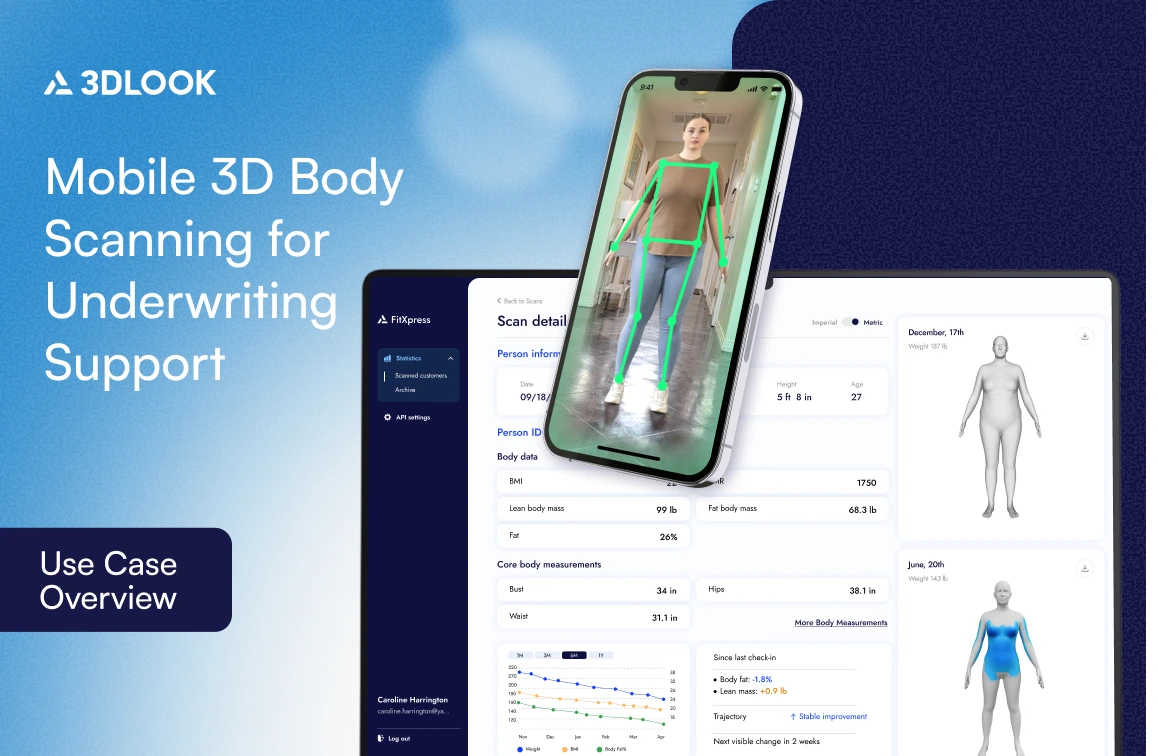

Where FitXpress Fits

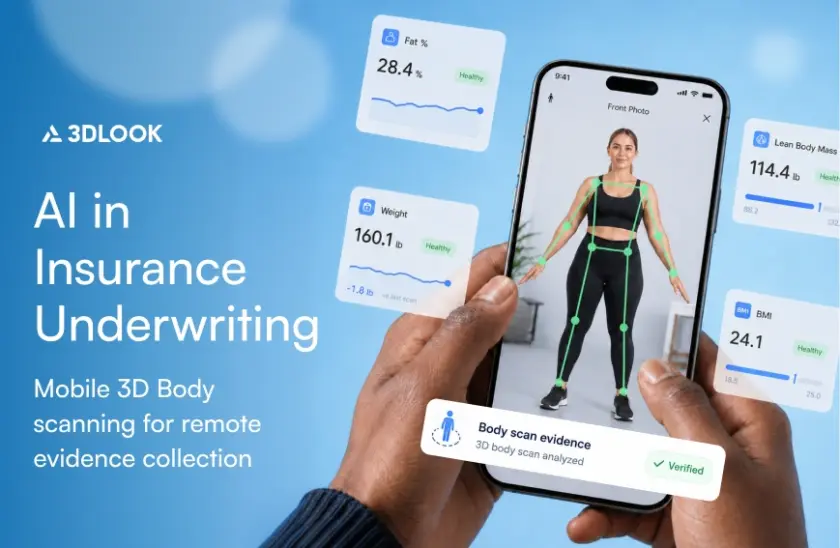

FitXpress by 3DLOOK enables insurers and digital distribution partners to collect structured body-related data remotely using a guided smartphone scan. Two photos and a ~45-second flow produce 80+ external body measurements, BMI insights, and weight prediction — outputs designed to support BMI/build verification, applicant triage, and fraud-prevention workflows without turning the technology into a standalone underwriting decision engine.

Throughout this article, we’ll show where in the underwriting process this kind of structured digital evidence delivers the most value — and where it should not be used.

Discover how AI-powered body intelligence is reshaping GLP-1 programs, telehealth, and digital health, from accurate remote assessments to safer and more engaging patient journeys.

What Is Insurance Underwriting?

Insurance underwriting is the process insurers use to evaluate risk, decide whether to accept an application, assign the applicant to an appropriate risk category, and set a premium that reflects that risk. The NAIC describes life insurance underwriting as the process of determining eligibility and classifying applicants into risk categories to set an appropriate rate.

Underwriters assess a combination of factors: health history, build, tobacco use, medications, lab results, financial information, and third-party records. Swiss Re describes this as building a data-based profile of each applicant using sources such as MIB records, prescription history, electronic health records, physician statements, physical exams, and lab reports.

Evidence quality is central to the process. If data is incomplete, inconsistent, or inaccurate, the insurer may assign the wrong risk class, price the policy incorrectly, or miss signs of misrepresentation.

How the Insurance Underwriting Process Is Organized

The sequence insurers follow to move from application to final coverage decision:

- Application. The applicant provides personal, financial, and coverage information, plus required disclosures and consent forms — including authorization to access medical records, prescription history, driving records, credit history, and financial statements.

- Evidence collection. In a traditional process, this can include a paramedical exam, blood or urine collection, attending physician statements, prescription database checks, MIB reports, and motor vehicle records.

- Risk review. An underwriter, AI, or rules-based system reviews the evidence against underwriting guidelines and determines the applicant’s risk class.

- Decision-making. Approving the application as submitted, offering different terms, requesting additional information, or declining.

Where Traditional Underwriting Slows Down

Manual evidence collection creates multiple handoffs, data requests, and follow-ups before an underwriter can begin a full review. Appointments and exams are another bottleneck: applicants may complete health testing within a few weeks and then wait several more weeks for the physician’s attending statement (APS) — after which the underwriter may still need clarification.

Traditional underwriting also relies heavily on applicant-provided information, which creates consistency issues. Self-reported health and body-related data are not always reliable: CDC researchers found that self-reported BRFSS data underestimated the overall prevalence of severe obesity by 40%. In life insurance underwriting, inaccuracies like these directly affect risk classification and pricing — and the problem compounds in remote workflows.

Why AI Matters in Modern Insurance Underwriting

AI helps insurers speed up underwriting without sacrificing review quality or regulatory discipline. It automates intake, improves consistency, and supports faster triage and review.

82% of companies using automated or accelerated underwriting reported reduced policy issue time. Average time to final decision: 9 days in automated programs vs. 27 days in traditional underwriting.

The benefits of integrating AI in underwriting:

- Reducing manual work to collect and process applicant information.

- Structuring evidence, surfacing key risk signals, and routing straightforward cases efficiently.

- Improving consistency by applying the same rules and checks across large volumes — flagging missing, insufficient, or inconsistent information.

- Separating fast-handling cases from those requiring deeper review or routing back to a full medical workup.

The strongest use case for AI is as a support tool for underwriters — not a replacement for or elimination of human judgment.

Use Case Overview: Mobile 3D Body Scanning for Underwriting Support

An applicant uses a smartphone to submit guided images. The system extracts a structured representation of external body shape and measurements — without a tape measure, a clinic visit, or a trained technician. The outputs support four practical stages: pre-screening, evidence collection, applicant verification, and workflow acceleration.

Where Mobile 3D Body Scanning Fits in the Underwriting Workflow

| Underwriting Stage | What Happens Today | How 3D Body Scanning Helps | Output for Underwriter |

|---|---|---|---|

| Pre-screening | Self-reported height/weight on application | Smartphone scan captures structured external measurements | Verified build data before full review begins |

| Evidence collection | Paramedical exam scheduled, lab work, APS requests | Remote, AI-driven measurement capture in minutes | Digital evidence file ready for triage |

| Applicant verification | Manual cross-check of disclosures vs. exam results | Automated comparison: disclosed vs. captured measurements | Flagged mismatches for closer review |

| Workflow acceleration | Every case follows a similar path until the exception triggers | Standard-risk cases routed faster; complex cases escalated | Faster decision on accelerated-eligible cases |

The Build & BMI Misrepresentation Problem

If there is one place where remote, structured body data delivers measurable value, it’s BMI and build. Munich Re reported in 2025 that changes in build and weight were the top reason for variances in risk class assessments in its accelerated underwriting analysis. BMI misrepresentation is the second-largest driver of misclassification in accelerated underwriting programs, after smoking non-disclosure.

Combined with the CDC finding that self-reported data underestimated severe obesity prevalence by 40%, the picture is consistent: build and BMI are simultaneously the most consequential body-related signals in underwriting and the most exposed to inconsistent reporting.

Mobile 3D body scanning addresses this directly. Smartphone-based imaging produces repeatable, machine-readable external body measurements that can be compared with applicant disclosures, turning a soft, self-reported field into structured digital evidence.

Traditional vs. AI-Assisted Underwriting with Mobile 3D Body Scanning

| Parameter | Traditional Underwriting | AI-Assisted + Mobile 3D Body Scanning |

|---|---|---|

| Time to the final decision | ~27 days on average | ~9 days in accelerated programs (LIMRA) |

| Body measurement collection | Paramedical exam, in-person, scheduled | Smartphone scan, remote, ~1–2 minutes |

| Data source for build/BMI | Self-reported + paramed measurement | Structured external measurements from 2 photos |

| Data consistency | Self-reported BMI underestimates severe obesity by ~40% (CDC) | Repeatable, machine-readable, standardized |

| Applicant friction | Multiple appointments, handoffs, follow-ups | Guided digital flow, no clinic visit required |

| Evidence auditability | Paper-based or fragmented digital records | Auditable digital trail per case |

| BMI misrepresentation exposure | High — #2 driver of misclassification (Munich Re) | Reduced via clothing detection + disclosure cross-check |

| Scalability | Limited by examiner availability and geography | Smartphone-native; scales across distributed populations |

| Best fit for | Complex / high-face-amount cases requiring full medical workup | Standard-risk cases on accelerated path (~59% per Gen Re 2025) |

Mobile 3D Body Scanning as a Fraud-Prevention Support Layer

According to the Insurance Information Institute, insurance fraud costs U.S. consumers an estimated $308.6 billion a year, including $74.7 billion in life insurance fraud. Better digital evidence supports fraud-prevention workflows at the underwriting stage by giving insurers a more structured way to compare what applicants disclose with what the workflow actually captures.

Mobile 3D body scanning does not solve every verification problem. The right way to position this technology is as a fraud-prevention support tool — not as a standalone fraud decision engine.

Fraud-Prevention Use Cases in Underwriting

- Flagging mismatches between disclosed and captured information. Any material gap between applicant disclosures and digitally captured body data may deserve closer review — especially when build or BMI influences risk classification.

- Supporting consistency checks across cases. Predictive approaches can identify applicants more likely to understate BMI and reroute higher-risk files to full underwriting for verification.

- Creating auditable digital records for review. When body-related evidence is captured digitally, insurers preserve a clear trail of what was collected, how it entered the file, and why a case was routed for further review.

Technology-level safeguards reinforce these workflows. To help identify attempts to manipulate scan outputs, 3DLOOK’s FitXpress includes built-in clothing detection — adding another layer of control to applicant verification.

Key Business Benefits for Insurers

- Faster underwriting cycle time. Move evidence collection and review into digital workflows without forcing every application through traditional verification. The 2025 Gen Re next-generation underwriting survey found that 59% of individual life insurance applications now qualify for an accelerated path.

- Better applicant experience with less operational friction. Fewer appointment-driven bottlenecks, fewer avoidable handoffs, and a workflow that matches how applicants actually want to buy coverage.

- More scalable evidence collection. Structured external body measurements through a smartphone workflow that deploys easily across distributed applicant populations.

- Stronger fraud prevention and consistent review. A consistent, auditable evidence source that helps surface discrepancies earlier and supports fairer case assessment.

Important Compliance Considerations

Accelerated underwriting models must be fair, transparent, based on sound actuarial principles, and monitored for unfair discrimination (NAIC). Transparent communication remains essential:

- Mobile 3D body scanning should be positioned as a non-clinical underwriting-support input — not a diagnostic tool or substitute for medical judgment.

- AI-driven 3D body scanning output should support underwriter review, not replace it.

- Privacy, consent, and data governance controls are equally important. Depending on jurisdiction, processing purpose, and implementation design, photos and body-derived outputs may be treated as personal, sensitive, health-related, or biometric data. Insurers should ensure appropriate consent, data minimization, retention, security, and governance controls.

- Decisions or actions made or supported by AI must comply with all applicable insurance laws and regulations.

3DLOOK’s FitXpress, powered by proprietary 3D computer vision, maintains HIPAA compliance and adheres to GDPR principles. Images are blurred, used only to generate scan results, and deleted immediately after processing. Data is encrypted in transit and at rest, with role-based access controls.

Conclusion

Mobile 3D body scanning gives insurers a practical way to modernize the underwriting process. As part of a broader AI-in-underwriting strategy, it helps carriers collect structured body-related data remotely, reduce dependence on appointment-heavy evidence gathering, and support faster initial review in life insurance workflows.

The business value is straightforward: more digital evidence, better workflow efficiency, expanded remote access, and more consistent inputs for verification and review. In a competitive market shaped by digital expectations, that is a meaningful operational advantage.

Next Steps

See how FitXpress can support remote evidence collection and BMI/build verification workflows in your accelerated underwriting program. Get in touch with 3DLOOK or book a demo to explore the technology in practice with our team.

FAQ

No. It supports evidence collection and review but does not replace required medical exams, lab work, or underwriter judgment. Final decisions remain with the insurer’s underwriting rules and human review.

It provides structured body-related data remotely, helping insurers compare applicant disclosures with scan-based outputs and route cases for review or fast handling — without requiring an in-person paramedical exam.

It should be positioned as a fraud-prevention support layer, not a standalone fraud detection engine. The technology helps flag mismatches between disclosed and captured body data, supporting the underwriter’s review process.

FitXpress captures 80+ body measurements from two smartphone photos in approximately 45 seconds, plus BMI insights, weight prediction, pose validation, and clothing detection — depending on the implementation.

FitXpress maintains HIPAA compliance and adheres to GDPR principles. Images are blurred, used only to generate scan results, and deleted immediately after processing. Data is encrypted in transit and at rest, with role-based access controls.

Approximately 45 seconds, using a guided two-photo flow on a standard smartphone — no special hardware, app installation, or trained technician required.